Table of contents

1. Employees should participate in the company in the long term?

Employee Participation | Company Participation | Company participation

Have you already thought about whether it makes sense for you to involve your employees at all and what they want to achieve with it? The next question is how exactly you can involve your employees – and what you should definitely consider.

In this part I will 6 very concrete (real) employee participation models introduce. From direct to indirect Employee equity participations with all its advantages and disadvantages. For me, special attention is paid to the legal form of the GmbH.

2. Direct participation as the ideal solution?

The most logical way to involve your employees in the success is certainly the direct participation in the company .

If the company operates successfully, the employee participates in the increase in the company's value (share price increase) and in annual distributions or dividend payments. As a shareholder, the employee has a direct influence on the result of his actions (no matter how small). In the best case, he even becomes an entrepreneurially minded employee.

But is direct participation also the ideal solution?

While this employee participation model is used in a listed "stock corporation" (AG) in the form of Stock option models (so-called ESOPS) and discounted employee shares, the widespread legal form of the "limited liability company" (GmbH) or the "entrepreneurial company" (UG) is faced with a dilemma here. But what are the opportunities to invest in companies?

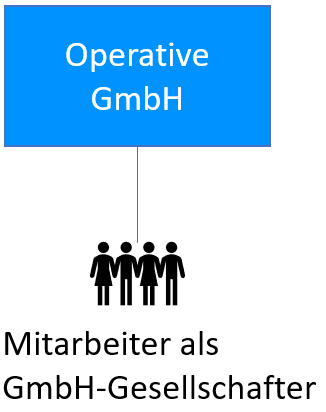

Option 1: Direct participation of the employees in the GmbH or UG

The GmbH or the "entrepreneurial company (haftungsbeschränkt", or UG for short, is the most widely used legal form in Germany after sole proprietors. The main reasons for this are the limitation of liability and the relatively simple incorporation. According to a Study by PwC from 2017, company founders choose the legal form of a GmbH or UG in 95% of all cases. Few founders have a direct stake in the company and the addition of a manageable number new (equity) investors, e.g. additional executives and investors, can be added relatively easily by means of a capital increase.

But what if you want to directly involve all or at least a large part of the employees in the GmbH? To put it bluntly, company participation is "difficult". Company law presents some head-breaking challenges here, as the legal form of the GmbH is not designed for a large number of people.

Here are just the biggest challenges:

Notarization (§15 GmbHG) and Publication every Change in shares in the commercial register. The procedure is therefore necessary for every new (involved) employee, including all costs incurred as a result.

Readiness of employees at the beginning of the activity ("up front") for a share of capital that is not valued on the market.

Possible solution may be via negative liquidation preferences .

Loss of necessary freedom of action , e.g. decisions only by convening all shareholders, regardless of the share

If necessary, no or only conflict-ridden possibilities to regain the share of capital when an employee leaves the company but wants to hold on to the stake.

Problem of the severance payment of departing shareholders. This often creates considerable potential for dispute, especially different views on the valuation of the share. [See also the article: Basic rules for an appropriate severance payment rule in the GmbH articles of association.

Due to these disadvantages, startups and increasingly grownups often make use of virtual employee ownership schemes (ESOPS and VSOPS), but these are more of a short- to medium-term nature and will be covered in Part 4 of this series.

For "long-established" GmbH's, direct employee participation in the GmbH/UG is only suitable for a small manageable number of employees, usually managers, for the reasons mentioned.

However, another way to involve a small number of executives can also be through corporate law structuring. In particular, taxation can be avoided here if necessary (see: Hurdle & Growth Shares – Avoidance of dry-income taxation through negative liquidation preferences? )

Another possible form of participation is the Convertible bond . We have covered these in a separate blog post: Company participation via convertible bonds | Convertible Loans – You should know these advantages and disadvantages!

EXCURSUS (Proposal Federal Association of German Startups e.V.)

The discrepancy between GmbH as the predominant legal form and the problem of employee participation are reasons why the "Bundesverband Deutsche Starttups e.V." together with the "Bosten Consulting Group" for a reform of the GmbH and tax law, which in particular provides for a simplification of employee participation. The study can be found here: Fair employee participation in startups – accelerating innovation and growth with entrepreneurial spirit

The main proposals of the study with regard to employee participation models are:

- Creation of a own asset class for employee participation. E.g. based on the model of the non-voting preference shares , which are issued cheaply, quickly and digitally, without notarization.

- Taxation of the employee only at EXIT Sale of the share and not at the time of allocation

- Tax-free net investment of income from employee shareholdings

- Simplified and transparent evaluation process of shares by the tax authorities, which provides for a discount of 40 – 60% from the last round of financing.

However, it could be years before such a reform takes place. Which proposals will ultimately be taken up is also still more than uncertain. Therefore, there is no other choice to make do with alternative options.

Update (December 2021)

As part of the Fund Location Act, it has been regulated since 1.7.2021 that the taxation of the share allocation can be deferred. In addition, the tax-free allowance has been increased from EUR 360 to EUR 1,440 per year from 1.7.2021. ( See the link to the German Bundestag). In the coalition agreement of the new "traffic light coalition", it was also agreed that this allowance should be increased again. If you are interested in the taxation of shares today, you should also read the following blog post: "What is taxed?" – Tax effect on share acquisitions and option models (ESOP|VSOP)

Option 2: Conversion into a stock corporation (AG)

The AG is certainly the most transparent model in the context of employee participation, as this legal form was designed precisely as a participation model. Of interest here, for example, is the structuring of the shares into ordinary shares with voting rights or non-voting preference shares, which give the shareholders the opportunity to retain control despite issuance. Nevertheless, the legal form of the AG is not a real option for many companies. Especially if a "regular" IPO is not planned or foreseeable in the near future.

Without this direct access to the capital market, it is almost impossible for smaller companies and their employees to sell shares or even determine a value for the capital share. The path over the Open Market would be a possibility, but (due to the tight market) it will not always lead to (appropriate) pricing when needed. There are also other reasons that deter many companies from setting up an AG, e.g.:

compared to the formation of a limited liability company higher share capital from 50.000 EUR (§7 AktG),

the installation of a Mandatory Supervisory Board (see §§95-116 AktG )

the obligation to hold a meeting at least once a year Annual general meeting and compliance with the invitation formalities so as not to be vulnerable.

if necessary complexes Accounting standards (IFRS) if an initial public offering (IPO) is planned, and

advanced Publication obligations .

These are all points that lead to higher personnel and financial expenditure without any immediate added value becoming visible.

Due to the additional external control by a supervisory board, the higher administrative costs and, in particular, the often missing market for the company's shares, a conversion into an AG is usually only advisable if a later IPO is planned and sufficiently concrete. Otherwise, however, the AG is currently the most consistent form of direct employee participation, especially if you include the structuring options, such as the issue of preference shares.

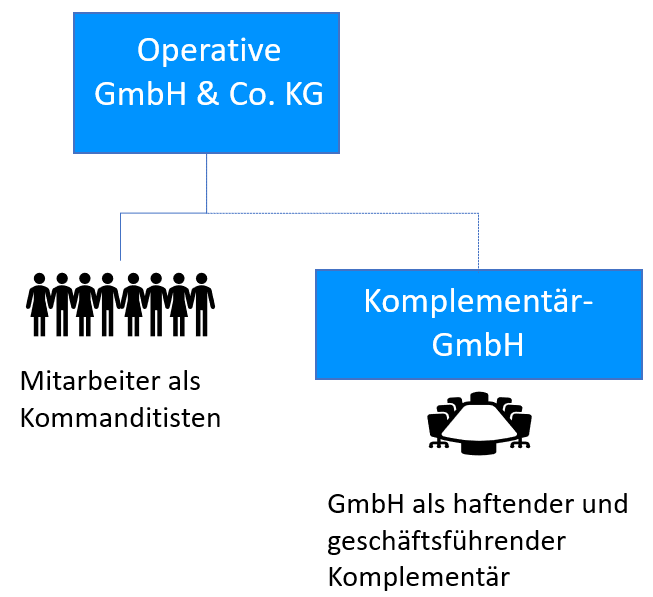

Option 3: The GmbH & Co. Medical history

An alternative could be the establishment or conversion of a GmbH into a GmbH & Co.KG, i.e. a partnership. The GmbH & Co.KG is particularly popular with Family business , since the distribution of assets of the limited partners is separate from the management by the general partner or general partner.

All of the above mentioned here, especially the advantages and disadvantages, of course also applies to employee participation in a limited partnership (KG). The only difference is the unlimited liability of the general partner.

The general partner retains control over the management of the company and the limitation of liability to the company's assets is retained by the GmbH. What works for family businesses could also be a solution for employee participation. In the general partner, the managing directors are employed accordingly, who can act in the same way as their GmbH participation. The employees participate in the company as limited partners and are only liable for the amount of their contribution.

any number of new limited partners can be admitted to the company, i.e. basically any employee.

Notarization is not necessary. However, the registration with the commercial register remains

the liability of the limited partners or employees is limited to their contribution (and other capital accounts, e.g. through profit allocation).

the limited partners participate in the company's success in accordance with their limited partnership contribution, receive distributions and participate in the increase in the value of the company.

(social) contractual provisions can also regulate the withdrawal from the KG. (For example, if an employee leaves the company, his entitlement to participation automatically expires and he is paid out accordingly. This ensures that only active employees participate in the company's success).

The employee will fiscal one Co-Entrepreneur , so that salary payments are included in profit income and no longer in income from employment. This means that the employee is then obliged to submit a corresponding tax return for business income himself, which is usually only possible with the support of a tax advisor and is therefore associated with considerable additional costs for the employee. In practice, this disadvantage usually weighs so heavily that direct participation in a GmbH & Co.KG no longer seems practicable with a large number of employees.

From now on, there are two companies and increased tax consulting costs. This consequently means increased administrative costs, e.g. for annual financial statements, accounting and tax returns.

The GmbH und Co.KG is a good instrument for the participation of manageable groups in the company and is therefore already used by many family businesses. However, when it comes to general employee participation, the tax reclassification from "income from non-self-employed work" to "income from commercial operations" usually weighs so heavily that it does not seem practicable.

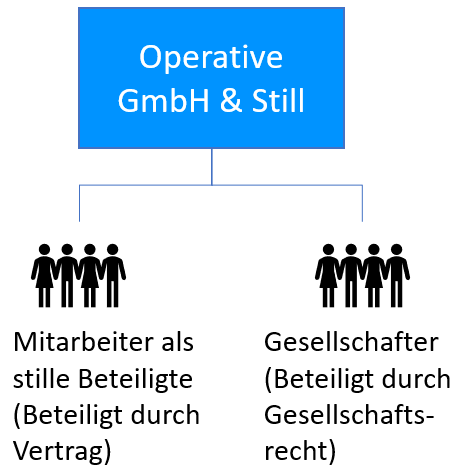

Option 4: Silent participation

The possibility of employee participation via a Silent participation (§§230 et seq. of the German Commercial Code) possibly in conjunction with a sub-participation. The silent partnership is an internal partnership between the owner/GmbH and the silent partner.

Since this internal society does not appear to the outside world, it is also called a "silent" society. In this case, the employee acquires a (silent) participation in the operating company through an asset contribution. If it is a GmbH, it is also referred to as a "GmbH und Still", which, however, does not correspond to a separate legal form.

It does not require a special form or notarial certification. Nevertheless, the written form is highly recommended, or in the case of co-determination in the company, it is factually indispensable in order to document the agreement in a legally secure manner.

The great advantage of the silent partnership is the high degrees of freedom in the structuring of the participation. Basically, all essential framework parameters can be contractually regulated and thus adapted to the individual case. For example, the contribution could also be made as a salary waiver or conversion of a bonus and thus become a component of the Corporate finance represent. A profit share would then no longer be distributed directly to the employee, but would remain in the company as a silent participation and strengthen the company's capital base.

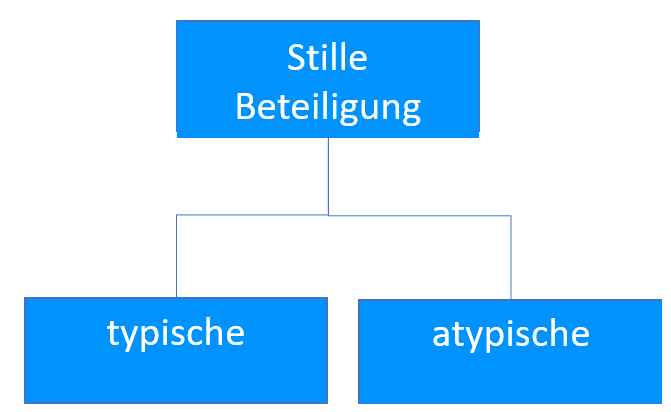

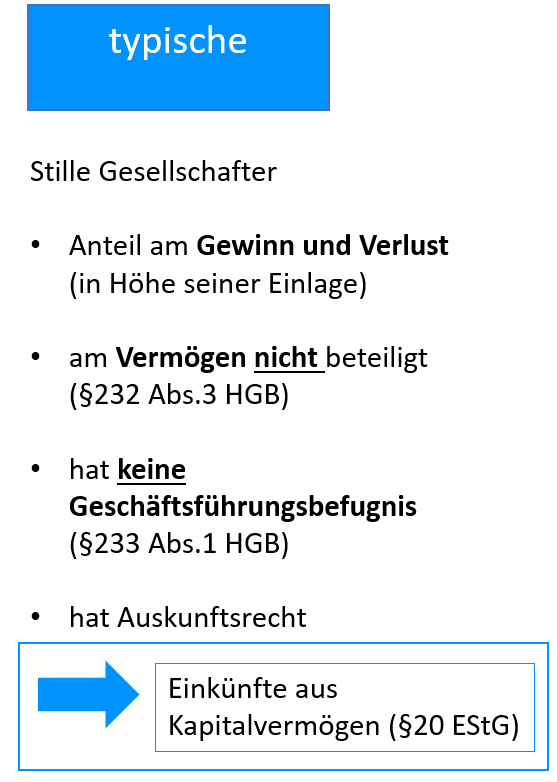

Distinction between typical and atypical silent partnership

Depending on the structure of the silent partnership, a distinction is made between typical and atypical silent partnerships. This distinction is very important because it has different legal and, above all, tax consequences.

The typical silent partnership is based on the legal requirements of the §§230 et seq. of the German Commercial Code (HGB) . Here, the shareholder is only a provider of capital and only interested in economic success (§231 para. 2 HGB) so Profit of the company through contribution. In terms of increases in value and thus in a later sale proceeds, on the other hand, the typical silent partner not part. Nor does he have any management authority, so that the "regular" shareholder retains his control rights to the full extent. For these reasons, the typical silent partner is treated like an investor for tax purposes and must "Income from capital assets" (§20 Abs.1 Nr.4 EStG) pay duty.

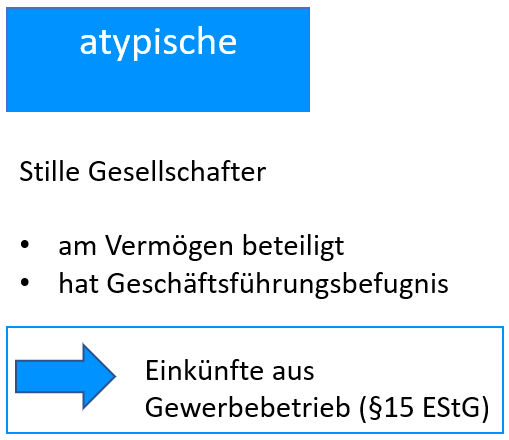

The atypical society deviates from the statutory provisions, e.g. when influencing shareholder decisions or participation in the company's assets. In the case of declaration as an atypical company, the shareholder becomes the Co-Entrepreneur and consequently has "income from commercial operations" (§15 para. 2 sentence 1 no. 2 EStG), i.e. like the limited partner.

The overview illustrates the differences once again:

EXCURSUS: Equity or Debt Capital? Structuring the silent partnership as mezzanine capital

For the company, the silent participation usually represents debt capital, unless it is structured as a so-called Mezzanine Capital , i.e. a mixed form of equity and debt capital. In this case, it is possible to report it in equity if the following criteria are cumulatively met:

- The silent partner's contribution is long-term and neither the business owner nor the silent partner can terminate at short notice. This is where the equity statement in the case of employee participation will usually fail. An employee or employer usually also wants to end the silent partnership when the employee leaves the company. Of course, something else could apply to managers and other key employees.

- In the event of the company's insolvency, the silent partnership must be a Subordinated action.

- The silent partner's contribution takes up to the amount of the deposit on the loss.

The advantage of classifying it as equity is obvious. The equity ratio will be higher and the bank's rating will improve accordingly. Borrowing via external lenders is correspondingly cheaper or even made possible by this.

High degree of freedom in the contractual design of employee participation

Low administrative effort (no notary or commercial register expenses)

Very easy admission of new shareholders, analogous to the workforce in an operational GmbH possible.

External financing by employees and strengthening of the capital base through possible retention of profits in the company

Advantages of financing when structuring as mezzanine capital (see EXKURS)

If classified as a typical silent partnership, employees have the option of the saver's allowance (§20 para. 9 EStG) .

Even if participation in losses is excluded, the silent partner is usually liable at least in the amount of his contribution. There is therefore a risk of a total loss for the shareholder, e.g. if he leaves the company.

In the case of employee shareholdings, stricter requirements for insolvency and deposit protection often apply, which must be met.

If structured as mezzanine capital, the employee takes a back seat to other creditors in the event of insolvency. So he is not only affected by the possible loss of his job, but also by a loss of assets.

In the case of the allocation of profit shares, capital gains tax must be registered and paid in the typical silent partnership for each partner who does not submit an exemption or non-assessment certificate (§43 para. 1 no. 3 EStG) . This can lead to increased administrative costs.

The typical silent partnership is a very good construct of employee participation due to the many degrees of freedom in the design and the possibility of alternative corporate financing. Nevertheless, there may also be reasons that can speak against a direct participation in a company. In most cases, this results from the analysis of the former shareholders prepared in Part 2 . For this reason, we are also looking at indirect participation via an employee participation company.

Option 5: Participation via profit participation rights and profit participation certificates

Due to its flexible structure, participation via profit participation rights & profit participation certificates can also be suitable for employee participation.

If you want to deal more intensively with profit participation rights, we refer you to the independent blog post here: Employee participation with profit participation rights & profit participation certificates: What you need to know!

This is also mezzanine capital and can be structured very similarly to the typical silent partnership. It can sometimes be difficult to distinguish it from typical silent partnerships. In its letter, the Federal Ministry of Finance BMF of 11.04.2023 – IV C 6 – S 2133/19/10004 :002 BStBl 2023 I p. 672 stipulates that no common purpose has to be pursued for a profit participation certificate.

Due to the similarity to the silent partnership, the advantages and disadvantages of profit participation certificates and rights apply analogously. We will therefore only go into special advantages and disadvantages here.

According to §3 No. 29 EStG, profit participation rights are Tax benefits . In addition, distributions and sales proceeds are considered income from capital assets and are therefore usually subject to the more favourable taxation of only 26.375% plus church tax.

The Embodiment of profit participation rights complex and thus costly be.

In the event of insolvency, profit participation rights are usually subordinate and the employee is threatened with a Total loss .

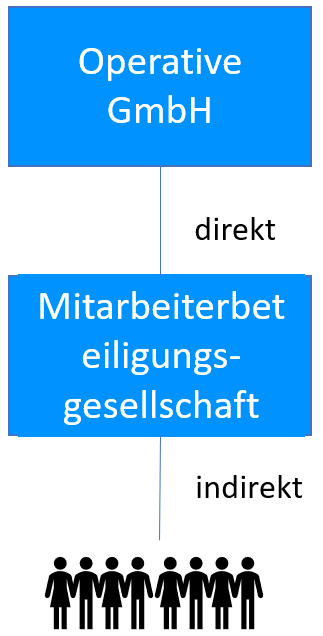

Option 6: Employee participation company

This employee participation model is an indirect participation. A Associated company and placed between the operative GmbH and the employees. The employee participation company has a direct interest in the original operating company. In practice, investment companies usually operate in the legal form of a GmbH or a "partnership under civil law" (GbR).

The main reason for such an intermediate company is the restriction of co-determination rights and the simplification of administrative burdens, as operating business and shareholdings are separated. "Information and control rights" and the "accounting of the investment accounts" are now more carried out in the investment company. However, the construct via an employee participation company can also be advisable for the following reasons:

If an existing shareholder wants to gradually reduce his share and successively transfers his shares to the investment company

If the investment company is to be open to an indefinite number of shareholders who are not yet known today.

When structural changes play a role. E.g. the separation of certain parts of the company from a company, the reduction of shares, for example to circumvent a consolidation obligation in the consolidated financial statements, etc.

The former owners determine the share with which they want the employees to participate in the operating company via the holding company and what share remains with the existing shareholders. In turn, the employees can participate in the investment company, e.g. within the framework of silent participation.

The employee company is basically a combination of a direct participation model and indirect employee participation.

The separation of operating company and participation can be a good construct for efficiently structuring employee participation.

EXCURSUS: Tax incentives for employee participation companies

The "employee participation" model has been taxed since 1 January 2024, by a Tax exemption (§3 No.39 EStG) up to 2,000 EUR/year promoted. Alternative Employee savings allowance from 20%on max. 400 EUR/year (§5VermBG ), which is usually less attractive than the tax exemption. The condition for this is:

- a spear period of at least 6 years on the contributions made by the employee ( see Federal Ministry of Finance )

- An income limit of EUR 20,000 for single persons and EUR 40,000 for married persons

All in all, very manageable amounts, but you should still think about them.

If you want to learn more about the topic, you can read the following blog article on the topic: "What is taxed?" – Tax effect on share acquisitions and option models (ESOP|VSOP)

Option 7: Virtual participation

The aforementioned problems, especially in the case of participation in a GmbH or UG (see option 1), have developed into another employee participation model in practice. This is often referred to as the "virtual participation model" because it fictitious participation under the law of obligations. In contrast to a real participation, however, this model is not explicitly regulated by law in company law, but is designed with the provisions of contract law. Because of this, it is up to the design itself how it wants to shape a virtual participation, with economic and tax implications.

Often, this virtual participation is also linked to options and is abbreviated as ESOP, vESOP or VSOP.

Since this is a very complex matter, we have covered it in a separate blog post:

ESOP, vESOP or VSOP? – Employee participation through options and virtual participations

3. Conclusion

As you can see, there are some differences in employee ownership models. Unfortunately, there is no standard model that fits every company. Depending on the goal you are pursuing, some models are better considered than others.

Therefore, make the Part 2: Analysis and make sure you consider all the essential points. Please feel free to take advantage of our free initial consultation

We are happy to find out what a cooperation can look like and how we can do it for you in a free and non-binding introductory meeting.

Duration: 30 min.