After the classic to the Company car taxation Today I would like to shed light on another "evergreen" of employee taxation:

The taxation of severance payments.

Especially since it will be incredibly difficult for the layman to understand how the fifths rule works. And this despite the fact that you can save considerable taxes with this regulation. In addition, I give a compact guide on where the information must be made in the tax return.

Table of contents

1. What is severance pay?

Severance pay is usually paid in direct connection with the loss of an employment relationship. This can be done on the basis of a voluntary agreement between employer and employee (termination agreement) or be the result of an employment law process after termination (settlement). The amount of the severance payment is freely negotiable. In practice, however, a value of 0.5 to 1 gross monthly salary per year of employment has become the benchmark. A labour judge will also be guided by this value (§1a para. 2 KSchG) .

The salary to be used as a basis is usually made up of all celebrate and variables components, e.g.:

- Gross salary

- Holiday and Christmas bonus

- Company car

- Other contractual commitments (pension schemes, subsidies, etc.)

- Target agreement and royalties (averaged over three years, if applicable)

Of course, it is in the nature of things that the interests diverge here. An employer will usually try to add as few salary components as possible. The employee, on the other hand, naturally tries to "knock out" the maximum possible. This is also where the greatest negotiation potential for both sides will lie.

2. How is the severance pay taxed? Save taxes through the one-fifth rule?

A severance payment is taxable as wages if it is received. In other words, like a normal monthly salary. In order to mitigate this tax burden, tax law, but a provision in §34 EStG ready. The so-called One-fifth rule (sometimes also written as a 1/5 rule). The Employer shall examine the one-fifth rule and apply it accordingly in payroll accounting.

PRACTICAL NOTE:

In practice, the Employer However, they usually do not have the necessary information for the assessment, so that in almost all cases the higher standard taxation is applied.

In order not to give away money, the employee has no choice but to apply for the Income tax return (§46 para. 2 no. 8 EStG) . I'll show you how to do that below.

3. Do I have to pay social security contributions on severance pay?

The good news: "No". In principle, no social security contributions have to be paid on a severance payment, if the severance pay is paid as "compensation" for the loss of the job. The severance payment may therefore be none Compensation for already "earned" entitlements, for example:

- sales commissions,

- Overtime or vacation entitlement

- Claims from target agreements or royalties, etc.

The same applies to the one-fifth rule. In practice, however, it will usually be difficult to assess a differentiation between the entitlement that has already been "earned" and the severance payment component. Especially if these components have not been contractually stipulated and are unambiguous. If it is unambiguous, however, a division will be made according to "regular earnings" and "severance pay".

4. What is the one-fifth rule?

Tax on severance pay – The one-fifth rule is difficult to understand even for tax specialists from the wording of the law. Would you like an example?

34 para. 1 sentence 2 and sentence 3 EStG

'The income tax to be assessed on extraordinary income shall be five times the difference between income tax on taxable income less that income (remaining taxable income) and income tax on the remaining taxable income plus one-fifth of that income. 3If the remaining taxable income is negative and the taxable income is positive, income tax shall be five times the income tax attributable to one-fifth of the taxable income.'

In principle, the aim is to Tax burden through a compensation payment mitigating . The severance payment is fictitious spread over 5 years, so to speak, and the applicable tax rate is reduced accordingly. Anyone who receives a severance payment and meets the following requirements can claim the one-fifth rule.

5. What are the prerequisites for the application of the one-fifth rule for income tax?

However, in order for the one-fifth rule to apply, a few prerequisites must be met, which have emerged from the administrative instructions and case law. The severance pay must be a Compensation act (§34 para. 2 no. 2 EStG iVm §24 No.1 EStG )

- than Compensation for lost or lost revenue .

This will usually be undisputed. However, as described above on social security contributions, care must be taken to ensure that these are not entitlements that have already been earned.

- must extraordinary income represent

The fact that the severance payment or compensation constitutes extraordinary income follows directly from the law (§34 para. 2 no. 2 EStG iVm §24 No.1 EStG )

- must clumped together flow to

It is important that the compensation flows in a "cumulative" manner, i.e. in a tax year, which leads to an increased tax burden.

IMPORTANT:

If a severance payment is spread over two or more assessment periods, the reduced taxation under the one-fifth rule is excluded (see Federal Fiscal Court, 21.3.1996 – XI R51/95) .

But there is also an exception here. If no more than 10% of the severance payment is postponed to the next year, this is "harmless" for reasons of simplification (see the BMF letter of 4.3.2016) .

6. How does the fifths rule work and how is it calculated?

The 1/5 rule is best applied to a small Example with calculation.

Taxing severance pay - examples

Example 1 - Mr. Max receives 25,000 EUR severance pay on 31.12.

Mr. Max is 50 years old, married and has 2 children (12 and 10 years old), tax class 4. Be Annual gross salary is EUR 48,000 . For the termination of his employment on 31.12. he receives a severance payment of 25.000 EUR .

| I | II | III | |

| Taxation without severance pay | Taxation with severance pay | Taxation with fifths rule | |

| Annual gross income | 48.000,00 | 48.000,00 | 48.000,00 |

| Compensation | 0,00 | 25.000,00 | 25.000,00 |

| Total income (taxable income) | 48.000,00 | 73.000,00 | 73.000,00 |

| Steer | 8.476,49 | 17.695,08 | 16.283,49 |

| Tax rate | 17,70% | 24,24% | 22,31% |

| Auxiliary calculation | |||

| Annual gross income without severance pay | 48.000,00 | ||

| + 1/5 of the severance payment of EUR 25,000 | 5.000,00 | ||

| Total Income | 53.000,00 | ||

| Taxes on this | 10.037,89 | ||

| Difference Tax III ./. Tax I | 1.561,40 | ||

| Tax difference between I and III multiplied by a factor of 5 | 7.807,00 | ||

| + Tax without severance pay (I) | 8.476,49 | ||

| Tax on fifths rule | 16.283,49 |

The sub-calculation shows how the one-fifth rule works. Only by applying them does Mr. Max save almost in our example 2% Taxes or 1.411,59 EUR .

So if his employer has not yet applied the one-fifth rule, Mr. Max can reclaim a nice amount with his income tax return and is a beneficiary.

Example 2 - Mr. Max takes a sabbatical and receives 25,000 EUR severance pay on January 1

After the exhausting year and the termination of his employment, Mr. Max wants to use the severance pay and treat himself to a year off (sabbatical). He agrees that the severance payment will only be on 1 January of the following year is paid out. So he has no further income in the following year.

| I | II | III | |

| Taxation without severance pay | Taxation with severance pay | Taxation with fifths rule | |

| Income | 0,00 | 0,00 | 0,00 |

| Compensation | 0,00 | 25.000,00 | 25.000,00 |

| Total income (taxable income) | 0,00 | 25.000,00 | 25.000,00 |

| Steer | 0,00 | 2.450,76 | 0,00 |

| Tax rate | 0,00% | 9,80% | 0,00% |

| Auxiliary calculation | |||

| Income without severance pay | – | ||

| + 1/5 of the severance payment of EUR 25,000 | 5.000,00 | ||

| Total Income | 5.000,00 | ||

| Taxes on this | – | ||

| Difference Tax III ./. Tax I | – | ||

| Tax difference between I and III multiplied by a factor of 5 | – | ||

| + Tax without severance pay (I) | – | ||

| Tax on fifths rule | – |

This example shows quite well the interplay between total income and the one-fifth rule. Due to the fact that Mr. Max does not earn any other income during his sabbatical and that the fifths rule reduces the amount below the Personal exemption his tax burden is reduced to EUR 0.00 in the following year. He can 2.450,76 EUR in the income tax return.

Example 3 - Mr. Max has negotiated well and will now receive 100,000 EUR severance pay on January 1 following year

Example 2 becomes even clearer if we assume that Mr. Max negotiated even better in order to "sweeten" his year off (sabbatical).

He now even gets EUR 100,000 Compensation on 1 January of the following year disbursed. So he has no further income in the following year.

| I | II | III | |

| Taxation without severance pay | Taxation with severance pay | Taxation with fifths rule | |

| Income | – | – | – |

| Compensation | – | 100.000,00 | 100.000,00 |

| Total income (taxable income) | – | 100.000,00 | 100.000,00 |

| Steer | – | 29.476,70 | 6.461,85 |

| Tax rate | 0,00% | 29,48% | 6,46% |

| Auxiliary calculation | |||

| Income without severance pay | – | ||

| + 1/5 of the severance payment of EUR 25,000 | 20.000,00 | ||

| Total Income | 20.000,00 | ||

| Taxes on this | 1.292,37 | ||

| Difference Tax III ./. Tax I | 1.292,37 | ||

| Tax difference between I and III multiplied by a factor of 5 | 6.461,85 | ||

| + Tax without severance pay (I) | – | ||

| Tax on fifths rule | 6.461,85 |

By the fact that the agglomeration takes place in the following year and Mr. Max does not earn any further income. If he only pays a tax rate of 6,46%, instead of the normal taxation rate of 29.48%. His tax savings are therefore 22.994,85 EUR .

Example 4 - Mr. Max has negotiated well, but will receive the 100,000 EUR severance payment on 31.12.

To complete the picture, let's now take a look at what it looks like if the same payout would be made on 31.12 of the tax year.

| I | II | III | |

| Taxation without severance pay | Taxation with severance pay | Taxation with fifths rule | |

| Income | 48.000,00 | 48.000,00 | 48.000,00 |

| Compensation | 0,00 | 100.000,00 | 100.000,00 |

| Total income (taxable income) | 48.000,00 | 148.000,00 | 148.000,00 |

| Steer | 8.476,49 | 50.565,04 | 44.152,59 |

| Tax rate | 17,70% | 34,17% | 29,83% |

| Auxiliary calculation | |||

| Income without severance pay | 48.000,00 | ||

| + 1/5 of the severance payment of EUR 25,000 | 20.000,00 | ||

| Total Income | 68.000,00 | ||

| Taxes on this | 15.611,71 | ||

| Difference Tax III ./. Tax I | 7.135,22 | ||

| Tax difference between I and III multiplied by a factor of 5 | 35.676,10 | ||

| + Tax without severance pay (I) | 8.476,49 | ||

| Tax on fifths rule | 44.152,59 |

Only one day of postponement from 1.1 subsequent year to 31.12 tax year results in a tax of 35.675,10 EUR compared to 6.461,85 EUR from example 3. So an additional burden of 29,214.25 EUR. Of course, these values are purely fictitious, as they are based on the assumption that Mr. Max will have no further income in the following year. However, this clearly shows the design possibilities offered by the one-fifth rule.

7. Claim the one-fifth rule in wage tax?

Of course, the one-fifth rule can also be applied to wage tax during payroll accounting. In the vast majority of cases, however, an attempt will be made to postpone the severance payment from tax structuring to the following year, so that it is subject to income tax with tax class 5. The difference can then be reclaimed as part of the income tax return (if you meet the requirements).

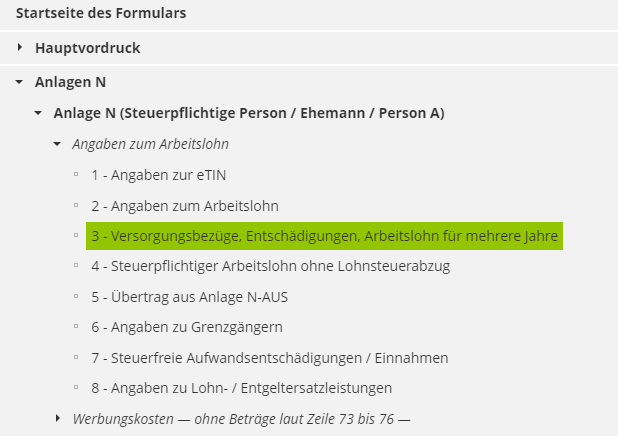

8. Where do I claim the one-fifth rule in my tax return?

Now for the most important part. Where do I actually make the fifths rule in my Tax return at the tax office?

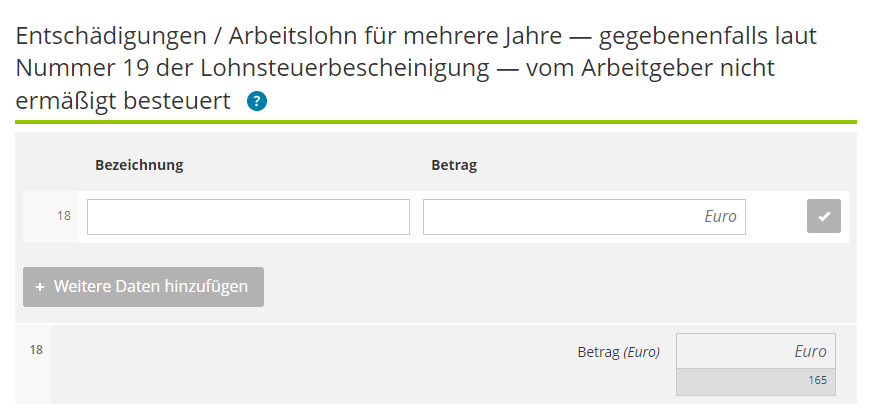

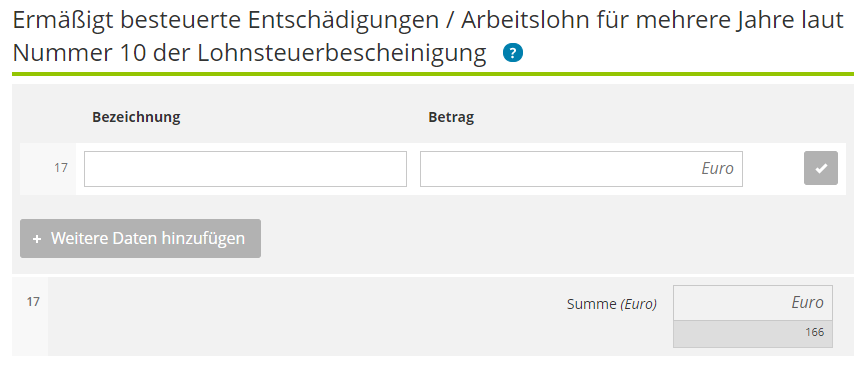

Easy. The Appendix N (non-self-employed work) of the income tax return, for example, the Line 18 or Line 17 ready:

We refer to the ELSTER form until 2019 and from 2020 to ELSTER Online or a common tax software.

Severance pay in the tax return form (2023)

The following information on severance pay and fifths rule can be found in the form for the income tax return in Elsteronline under number 3.

LINE IN THE ELSTER FORM (until 2019)

HINT:

However, the prerequisite for this is that the Employer has correctly stated the severance payment or compensation in advance in the wage tax certificate (eTin):

LINE IN ELSTERONLINE (from 2020)

From 2020, the parental form will be history and you have to prepare the income tax return via the Elster portal. However, the information is identical and looks a little different:

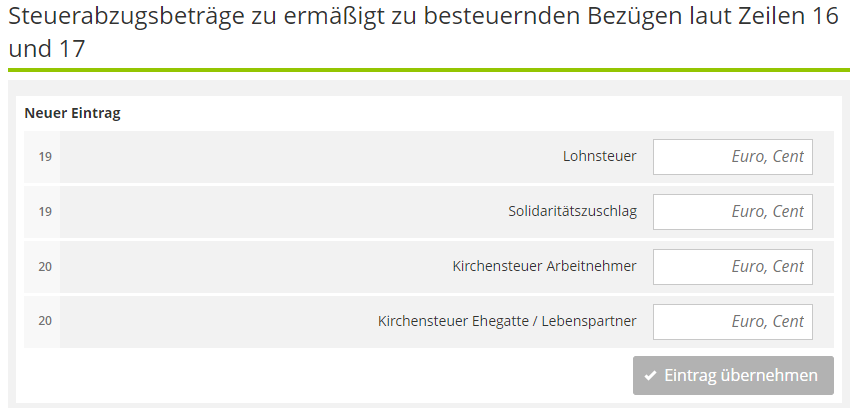

If the employer has correctly stated the compensation and correctly stated the tax on the wage tax certificate, then line 17 + line 19 must be filled in. This will be the Rule but must still be checked in advance.

ZEILE IN ELSTERONLINE (2021)

By the beginning of January 2022, no new forms were available in ElsterOnline. However, we assume that these will follow in the next few weeks and that the lines will not change or will not change much.

9. Conclusion

As you have seen, the one-fifth rule can reduce the tax burden for severance pay in some cases considerably. Examples 3 and 4 show that there is also considerable room for manoeuvre here. If the employer has not yet applied the one-fifth rule in the payroll, you should use it unconditional in the context of the income tax return as shown here. In this way, you can save taxes with your severance pay.

On the subject of severance payments, I also refer to the article: Thinking about the end at the beginning? 3 Basic rules for an appropriate severance payment provision in the GmbH articles of association

We are happy to find out what a cooperation can look like and how we can do it for you in a free and non-binding introductory meeting.

Duration: 30 min.